MMM for Financial Services: Banking & Insurance Guide

Discover how marketing mix modeling financial services solves attribution challenges, optimizes budget, and navigates privacy regulations. Read the full guide.

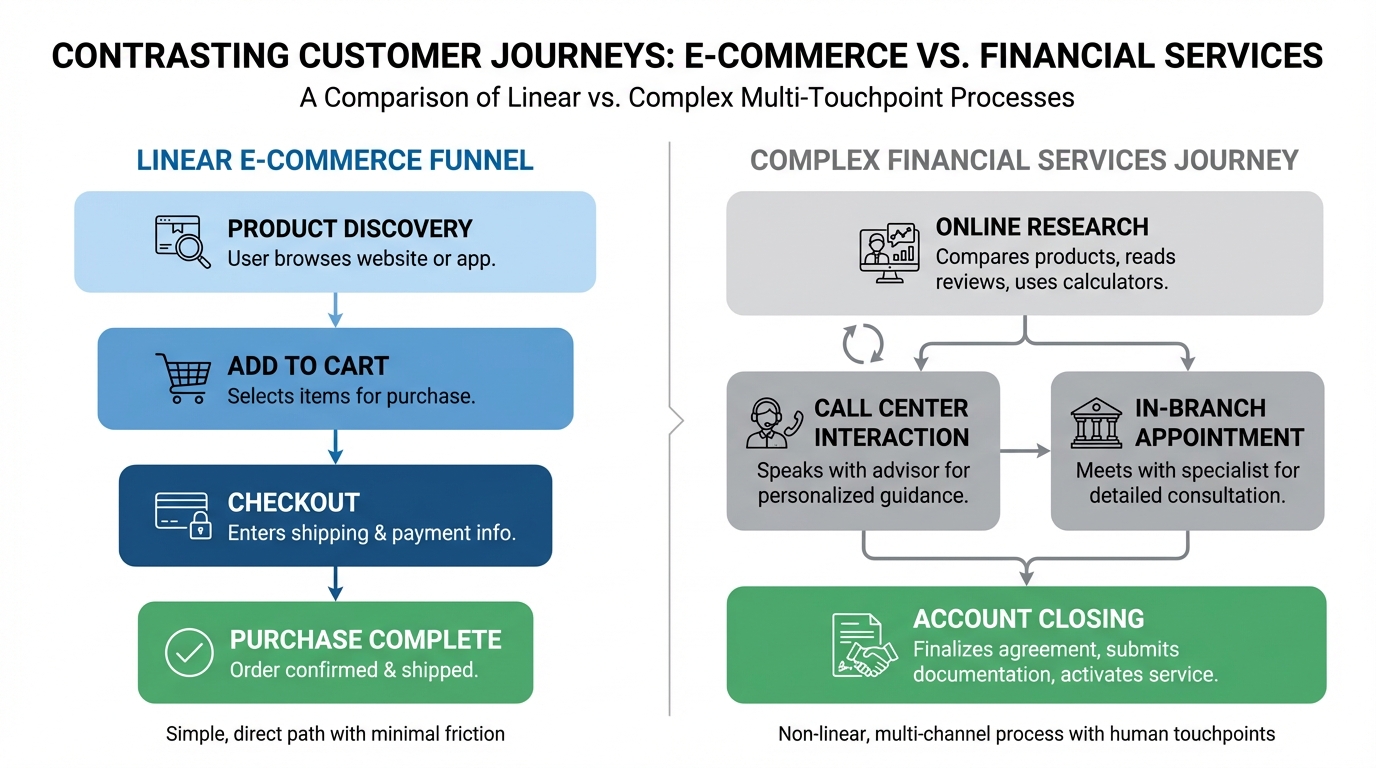

Marketing in the financial sector is brutal. You deal with long sales cycles, complex customer journeys, and strict regulatory hurdles. A customer might see a Facebook ad for a credit card today but apply in a branch three weeks later. Traditional tracking pixels break down completely in this environment.

This is where marketing mix modeling financial services becomes essential.

Unlike retail or e-commerce, where the path to purchase is often linear and digital, financial services operate in a hybrid world. You have data silos between your digital team, your branch network, and your call centers. Relying on click-based attribution tells you less than half the story.

This guide breaks down exactly how banks, insurers, and fintechs use Marketing Mix Modeling (MMM) to measure what actually drives revenue—without violating privacy laws or guessing at offline conversions.

The Attribution Problem in Finance

If you work in marketing for a bank or insurance firm, you know the pain of "last-click" bias. A user searches for "best mortgage rates," clicks your Google Ad, and applies. Google takes 100% of the credit.

But that user likely saw your TV spot, read a blog post, and received a direct mailer two months ago.

Financial products require trust. Trust takes time to build. By ignoring the upper-funnel interactions, you undervalue brand building and overspend on bottom-funnel search ads. This inflates your Customer Acquisition Cost (CAC) and stifles growth.

{kind=link}

To fix this, you need a measurement framework that looks at the big picture. You need to understand how different channels interact to drive conversions. For a deeper dive into how this differs from tracking individual clicks, read our guide on media mix model marketing attribution.

Why Cookies Fail Finance

Privacy regulations like GDPR and CCPA hit financial services harder than most industries. You handle sensitive financial data. Using third-party cookies to track users across the web is becoming impossible and legally risky.

MMM solves this. It doesn't track individuals. It uses aggregated data to find statistical relationships between marketing spend and business outcomes. It is privacy-safe by design.

According to a report by McKinsey, companies that integrate advanced analytics like MMM can see a 15-20% increase in marketing ROI. For a major bank, that percentage represents millions in saved budget.

Marketing Mix Modeling Financial Services: Sector by Sector

Not all financial institutions are the same. A neobank has different data challenges than a 100-year-old insurer. Here is how MMM applies to specific verticals.

1. Banking: Bridging Digital and Branches

For retail banks, the biggest blind spot is the branch. You spend millions on digital ads, but a significant portion of new accounts still open in person. According to the American Bankers Association, while digital usage is high, older demographics and high-value loan applicants frequently prefer physical branches for final decisions.

MMM ingests data from all sources. You feed the model:

- Digital ad spend (Facebook, Google, LinkedIn)

- Offline spend (TV, Radio, OOH)

- Branch foot traffic

- New account openings (online and offline)

The model calculates the lift. It tells you, "For every $1,000 spent on YouTube in Chicago, branch visits increased by 15%."

This holistic view allows you to defend your branding budget. When the CFO asks why you are spending on "untrackable" channels, you show them the statistical correlation to revenue.

If you are currently debating between different measurement approaches, check out our MTA vs MMM comparison to see why banking leaders are shifting toward MMM.

2. Insurance: The Agent and Aggregator Dilemma

Insurance marketing is fragmented. You have direct-to-consumer digital channels, independent agents, and aggregators (comparison sites).

Agents often run their own local marketing. Aggregators own the customer data until the lead is sold. Research from Deloitte highlights that insurers must increasingly rely on advanced analytics to decouple these complex distribution channels and understand true profitability.

Marketing mix modeling financial services allows insurers to measure the incremental impact of national brand campaigns on local agent performance. It helps answer critical questions:

- Does national TV advertising lower the CPA for local agents?

- Are aggregator leads cannibalizing organic traffic?

- What is the true ROI of sports sponsorships?

By analyzing these variables, insurers can optimize their media mix to support the most profitable distribution channels.

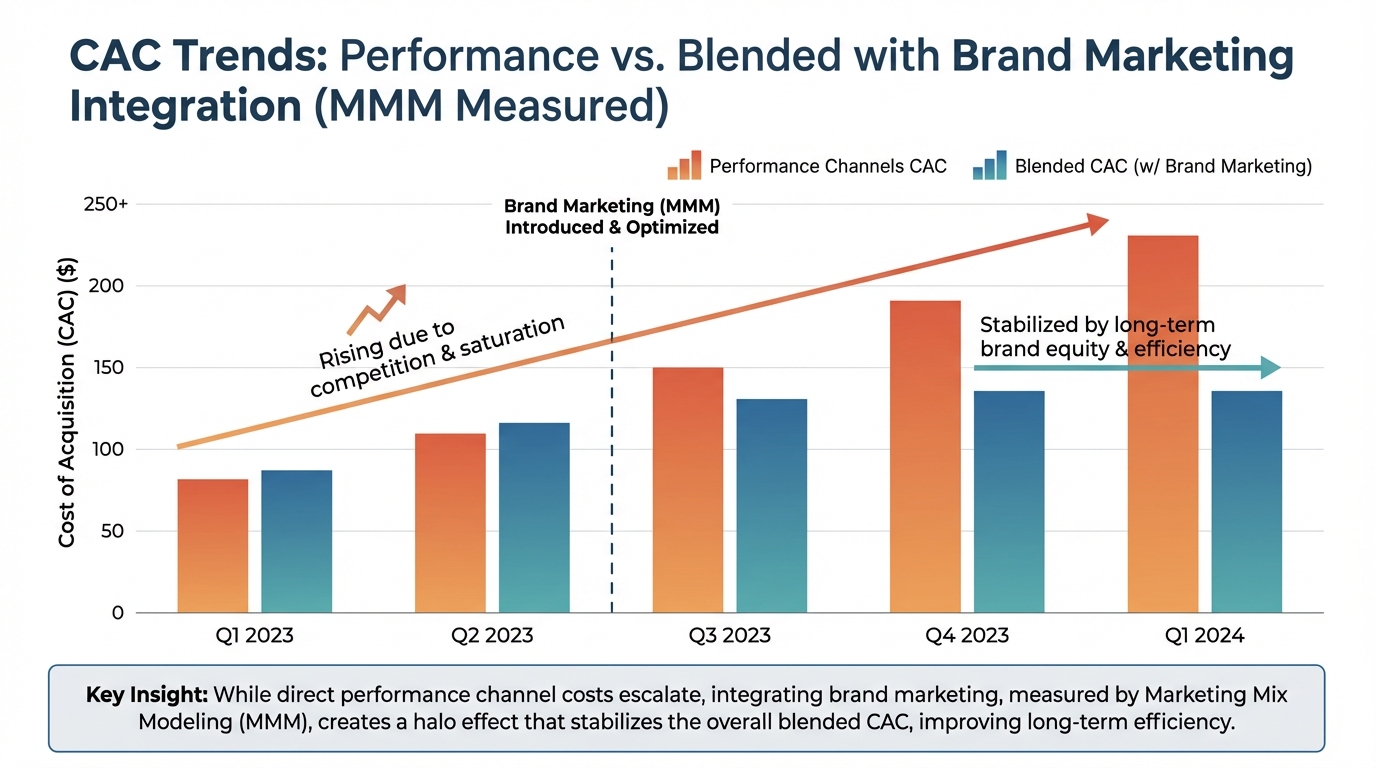

3. Fintech: Scaling Beyond Performance Marketing

Fintechs usually start with pure performance marketing. It works well until you hit a growth plateau. To scale, you eventually need brand marketing—podcasts, influencers, billboards.

The problem? You can't track a billboard click.

According to investment firm a16z, relying solely on paid acquisition without organic brand lift eventually destroys unit economics. Fintechs use MMM to measure the "halo effect" of brand spend. When you launch an Out-of-Home (OOH) campaign in New York, does your organic search volume spike? Does your paid search conversion rate improve?

[IMAGE: Bar chart showing the cost of acquisition (CAC) rising over time for performance channels, while blended CAC stabilizes after introducing brand marketing measured by MMM.]

Alt text: Chart demonstrating how brand marketing stabilizes blended CAC in fintech growth stages.

!Chart demonstrating how brand marketing stabilizes blended CAC in fintech growth stages.*

{kind=link}

Critical Variables for Finance MMM

A generic model won't work for finance. You must account for external factors (covariates) that influence money movement. If you ignore these, your model will be inaccurate.

Interest Rates

This is the single biggest driver for lending products. If the Federal Reserve cuts rates, mortgage applications will skyrocket regardless of your ad spend. You can track these trends directly via the Federal Reserve Economic Data (FRED). Your model must control for interest rates to isolate the true impact of your marketing.

Seasonality

Tax season drives IRA contributions. The holidays drive credit card usage. January drives debt consolidation loans. Your MMM must factor in these predictable seasonal spikes.

Economic Confidence

Inflation and consumer sentiment scores affect investment products. When confidence is low, people hoard cash. When it's high, they invest.

By including these variables, you get a clean read on marketing performance. This is the core of marketing effectiveness measurement.

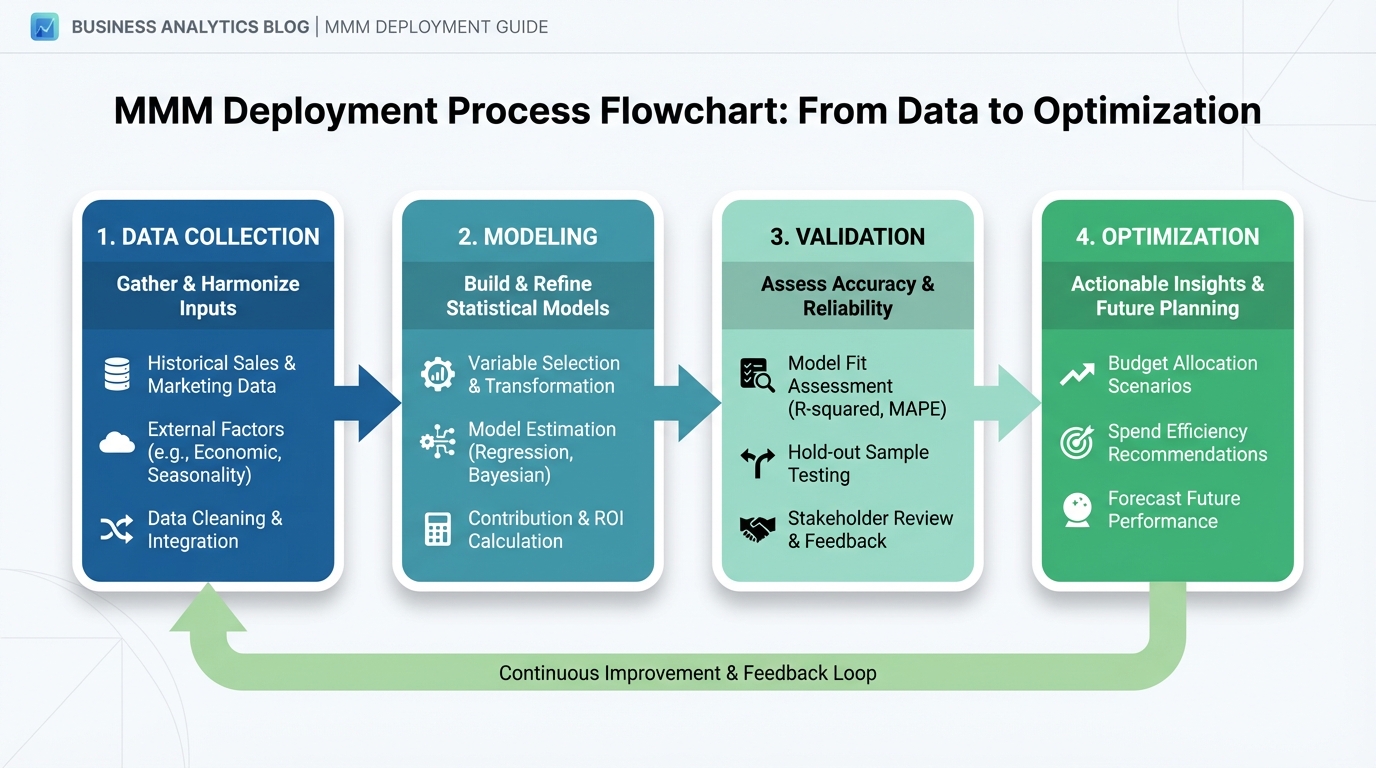

How to Deploy MMM in Financial Organizations

Implementing MMM in a regulated environment requires a structured approach. You cannot simply upload customer data to a public cloud without security reviews.

Step 1: Data Unification

Gather data from your ad platforms, CRM, and core banking systems. This is often the hardest part. You need weekly or daily data going back at least two years.

Step 2: Model Selection

You have three choices:

- Consultancies: Expensive and slow. Good for one-off audits.

- Open Source: Libraries like Google Meridian or Meta Robyn. These require a dedicated data science team.

- SaaS Platforms: Solutions like BlueAlpha that automate the modeling process.

For most financial teams, speed is critical. Building an internal model can take six months. SaaS platforms can deliver results in weeks.

Step 3: Validation and Calibration

Test the model. If the model says TV ads drive 20% of conversions, run a lift test. Turn off TV in one region and see if conversions drop by the predicted amount.

For a detailed roadmap, read our guide on how to deploy a media mix model.

[IMAGE: Flowchart illustrating the MMM deployment process: Data Collection -> Modeling -> Validation -> Optimization.]

Alt text: Step-by-step process for implementing marketing mix modeling in a financial institution.

Caption: A structured deployment ensures your model delivers actionable insights, not just data.

!Step-by-step process for implementing marketing mix modeling in a financial institution.*

{kind=link}

The goal of marketing mix modeling financial services isn't just to report numbers. It's to optimize future spend.

Once your model is running, you can run "what-if" scenarios.

What happens if I cut search spend by 10% and move it to YouTube?*

What is the saturation point for Facebook ads?*

Financial marketers often find they are overspending on branded search (bidding on their own bank name) and underspending on video. MMM gives you the confidence to shift that budget.

According to Harvard Business Review, companies that actively reallocate budget based on data can improve efficiency by up to 30%.

To understand how to execute these shifts effectively, check out our media budget optimization guide.

Comparing MMM Platforms for Finance

Choosing the right tool is difficult. Financial services require enterprise-grade security and the ability to handle complex covariates.

BlueAlpha vs. The Rest

BlueAlpha is designed for modern marketing teams who need answers fast. It handles the complex data integration required by banks and insurers while offering the transparency of open-source models.

Many legacy platforms operate as "black boxes"—you put data in, you get a report, but you don't know how the math worked. In finance, you need explainability. You need to be able to explain to the Risk Committee exactly how the model reached its conclusion.

If you are evaluating tools, it helps to see how they stack up.

Legacy tools like Keen Decision Systems have been around a long time, but often lack the agility required for modern digital channels. Newer AI-driven platforms provide faster insights.

For a broader look at the landscape, you can explore Keen Decision Systems alternatives or Lifesight alternatives.

Navigating Regulatory Compliance

Compliance is the elephant in the room.

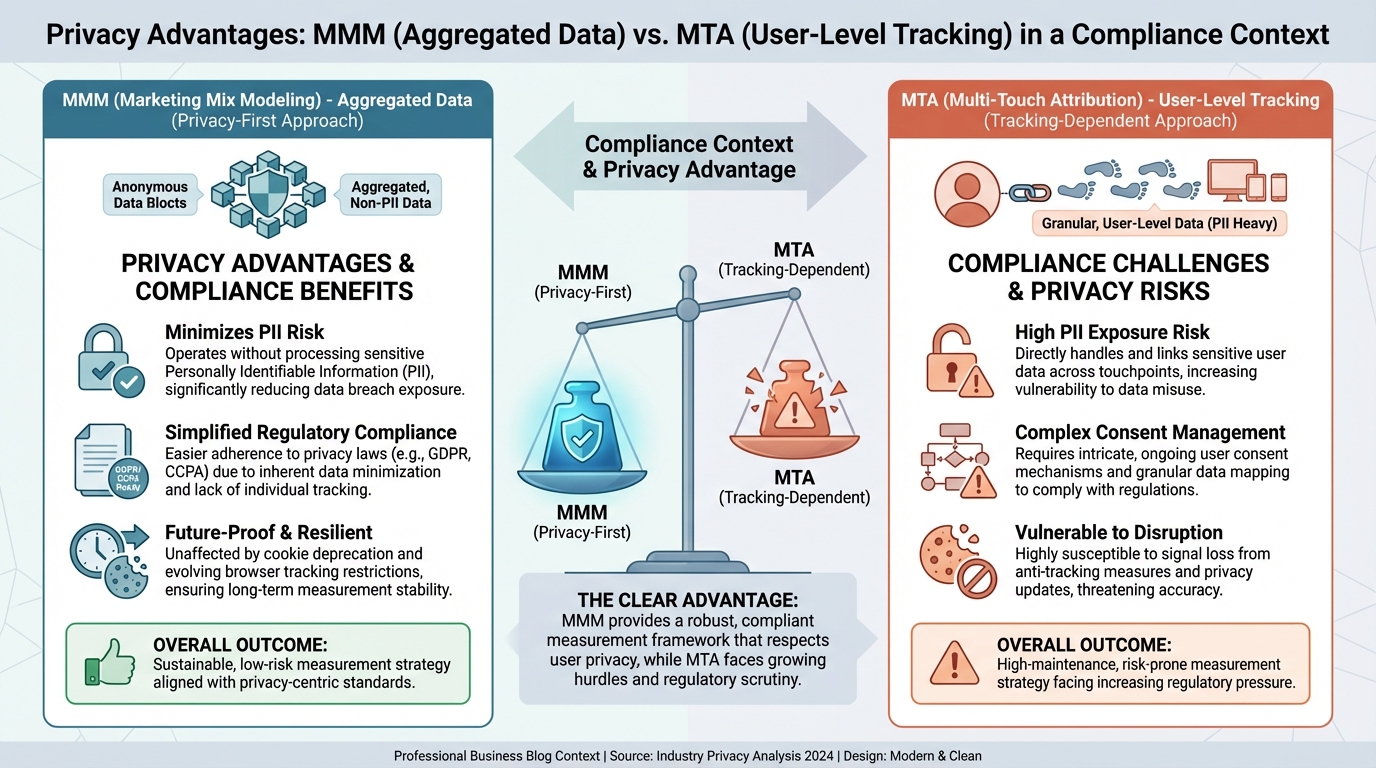

Marketing mix modeling is inherently safer than multi-touch attribution (MTA) because it does not rely on User-Level Data (ULD). You are not tracking John Smith's mortgage application. You are tracking total mortgage applications in the Northeast region.

However, you still need to ensure your data handling meets internal standards. The GDPR.eu official guide outlines strict principles for data minimization, which MMM naturally adheres to by using aggregated datasets rather than individual identifiers.

- Data Aggregation: Ensure all data export scripts aggregate data before it leaves your secure environment.

- Vendor Security: Choose MMM vendors with SOC 2 Type II compliance.

- Model Explainability: Regulators (and internal auditors) dislike black-box AI. Ensure your model offers transparency into coefficients and logic.

[IMAGE: Infographic showing the privacy advantages of MMM (aggregated data) vs. MTA (user-level tracking) in a compliance context.]

Alt text: Comparison of data privacy safety between MMM and Multi-Touch Attribution.

Caption: MMM minimizes compliance risk by relying on aggregated data patterns.

!Comparison of data privacy safety between MMM and Multi-Touch Attribution.*

{kind=link}

Calculating ROI in finance is tricky because of Customer Lifetime Value (CLV). A checking account might lose money in year one but generate profit for 20 years.

Your MMM should not just optimize for "Cost Per Lead" (CPL). It should optimize for predicted revenue.

By integrating LTV data into your model, you can distinguish between "cheap" leads that churn quickly and "expensive" leads that become loyal banking customers.

For a deep dive into calculation methods, refer to our marketing ROI analysis guide. Furthermore, if you are targeting high-value commercial clients, our ABM ROI measurement guide is essential reading.

FAQ: MMM in Financial Services

Q: Can MMM measure the impact of branch signage?

A: Yes, if you have historical data on when signage was changed or updated. However, it is easier to measure broader offline channels like OOH or local radio.

Q: How much historical data do I need?

A: Ideally, 2-3 years of weekly data. This allows the model to detect seasonality and long-term trends.

Q: Does MMM replace Google Analytics?

A: No. Google Analytics is for tactical, real-time website monitoring. MMM is for strategic budget allocation and measuring total marketing effectiveness.

Q: Is MMM expensive?

A: Traditional consulting engagements cost hundreds of thousands. Modern SaaS solutions like BlueAlpha are significantly more affordable and faster to deploy.

Q: How do we handle B2B banking products?

A: B2B cycles are longer. You need to account for pipeline stages. See our guide on pipeline attribution for specifics on B2B modeling.

Conclusion

The financial services landscape is changing. Third-party cookies are dying. Regulators are watching. Competition from agile fintechs is increasing.

Old-school attribution methods leave you flying blind. Marketing mix modeling financial services provides the radar you need to navigate these challenges. It connects your offline and online worlds, respects user privacy, and provides mathematical proof of what works.

Don't let your budget go to waste on channels that claim credit they didn't earn. Start building a model that reflects the reality of your business.

Ready to see which model fits your needs? Read our comparison on which MMM is best to take the next step.